Profit and Loss Statement for Small Business: A Hanover, PA Guide to Financial Clarity

Profit and Loss Statement for Small Business

What if the 15 minutes you spend reviewing a single report could save your Hanover business $4,350 in unnecessary expenses this year? Data from a 2023 small business survey shows that 62% of owners feel "blind" to where their money goes, even after working 55 hours a week. Mastering a profit and loss statement for small business isn't about becoming a math genius; it's about finally seeing the truth behind your hard work. You likely started your company to serve the community, not to get buried under a pile of receipts or confusing terms like COGS and Gross Margin.

It's completely normal to feel that familiar sting of anxiety when your CPA asks for reports you haven't finished yet, but we're here to turn that chaos into a sense of "thank heavens" clarity. You'll learn how to transform raw data into a professional report that provides total peace of mind and the confidence to make smarter decisions. This guide will walk you through reading your P&L, simplifying the terminology, and using those insights to build a more profitable future for your business.

Key Takeaways

- Understand your financial "scoreboard" to clearly differentiate between what your business owns and what it actually earns over time.

- Master the anatomy of a profit and loss statement for small business to see the vital difference between your gross revenue and your final net income.

- Learn how to spot hidden "money leaks" and track growth trends that turn your local business data into clear, actionable strategies.

- Follow a simple five-step process to organize your income and expenses, moving you from financial overwhelm to total clarity.

- Discover how professional bookkeeping provides the "Thank Heavens" relief and confidence you need to focus on your business’s future.

What is a Profit and Loss Statement and Why Does Your Hanover Business Need One?

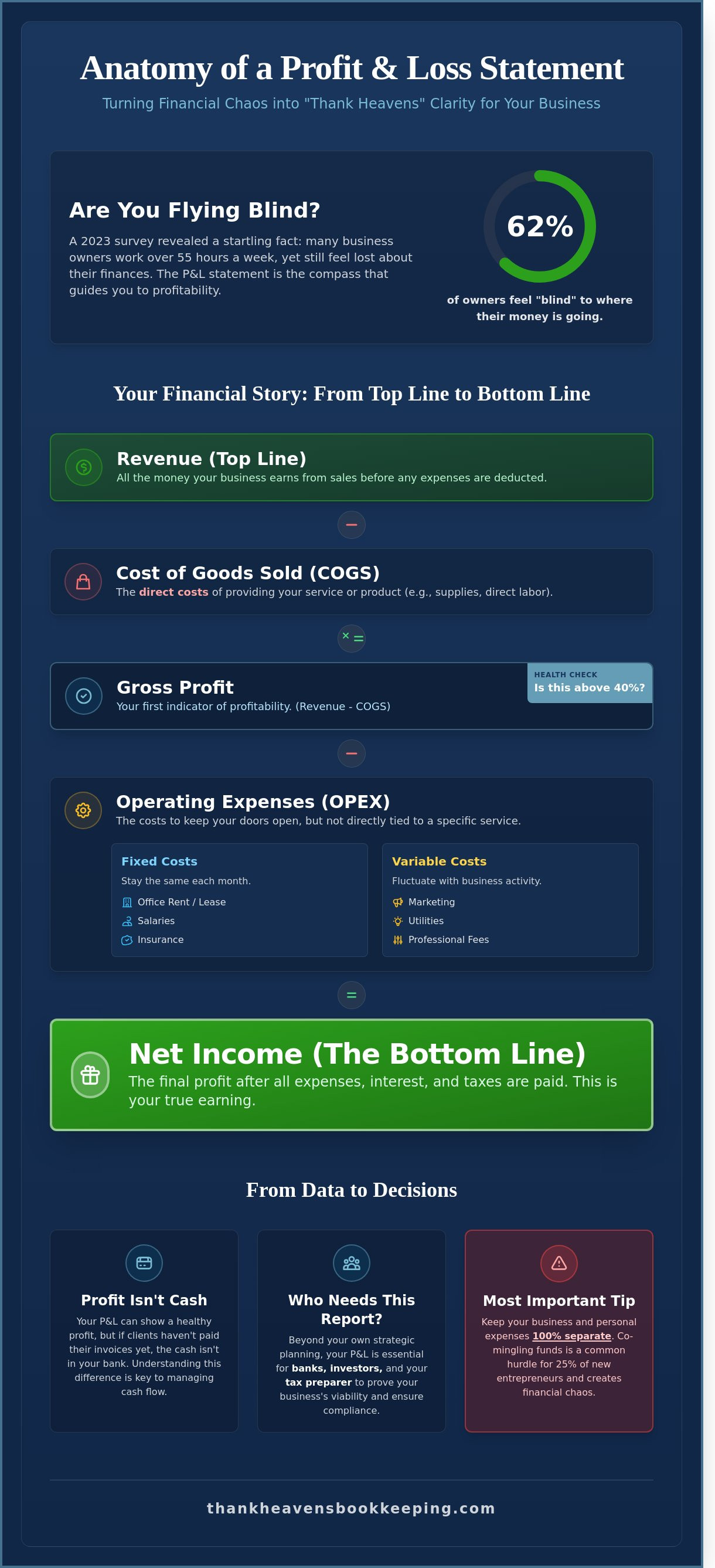

Running a business in Hanover shouldn't feel like wandering through a fog. A profit and loss statement for small business, often called a P&L or Income Statement, acts as your financial scoreboard. It tracks your total revenue and subtracts every expense over a specific window of time, such as the 2024 fiscal year or a specific quarter. While a Balance Sheet provides a snapshot of what you own and owe at a single moment, the P&L tells the story of your operations over a duration. It reveals exactly how your hard work translates into actual earnings.

Think of this document as your financial sanctuary. When your books are organized, the chaos of receipts and invoices transforms into a clear narrative of success. Local Hanover lenders and the IRS require this report because it proves your business is a viable entity. If you apply for a commercial loan at a bank in York or Harrisburg, they'll look at your P&L first to see if you can cover the debt. Without this clarity, you're essentially flying blind, which adds unnecessary stress to your already busy life.

The Difference Between Profit and Cash in the Bank

You might see a healthy bottom line on your report and still wonder why your bank account looks low. This happens because profit and cash aren't the same thing. If you invoiced a client for $5,000 on a 30-day cycle, that "profit" shows up on your P&L immediately, but the actual cash won't hit your bank for another month. You also have to consider loan principal payments or equipment purchases that don't always appear as traditional expenses. Looking beyond the bank balance allows you to see the true health of your business. It gives you the confidence to know that while the cash is tied up today, your foundation is solid for tomorrow.

Who Needs to See Your P&L Statement?

Several people rely on your financial reporting to help your business thrive. Internally, you need this data to make smart choices. If you're considering hiring a new team member in 2025, your P&L shows if you have the consistent margin to afford them. Externally, your tax preparer uses this document to ensure you're taking every legal deduction possible. Banks and investors also require these statements to gauge your risk level. If you feel overwhelmed by the numbers, partnering with a bookkeeper in Hanover, Pennsylvania can provide the relief you need. We handle the meticulous details so you can focus on the work you love, knowing your financial house is in order.

The Anatomy of a P&L: Breaking Down Revenue and Expenses

Looking at a profit and loss statement for small business for the first time can feel like staring at a puzzle with a thousand pieces. However, once you understand the top-down structure, that confusion turns into immediate relief. Think of your P&L as a story that starts with your hard work and ends with your reward. It moves from the "Top Line," which is your total Gross Revenue, down to the "Bottom Line," or your Net Income. Seeing your numbers organized into these 15 to 20 standard categories provides a sense of calm that chaotic spreadsheets simply can't offer. It's the moment you stop guessing and start knowing.

For service-based businesses, distinguishing between fixed and variable costs is vital for long-term health. Fixed costs, like a $1,500 monthly office lease in Hanover, stay the same regardless of your client load. Variable costs fluctuate based on your activity. When you see these separated clearly, you gain the freedom to make decisions based on facts rather than fear. You'll finally see exactly where your hard-earned money goes each month.

Understanding Revenue and Cost of Goods Sold (COGS)

COGS represents the direct costs required to deliver your specific service or product. If you run a local cleaning service, this includes the supplies and labor used for a specific job. To find your Gross Profit, subtract your COGS from your total revenue. This margin is your first indicator of viability. If your Gross Profit margin is sitting below 40%, it's a signal that your pricing or production costs need a gentle adjustment to ensure your business remains sustainable and profitable.

Operating Expenses and Other Income

Operating expenses are the costs of keeping your doors open every day. This list typically includes your marketing budget, professional fees, and utilities. These are distinct from "Below the Line" items like interest payments or taxes, which are calculated after your operating income is determined. One of the most important steps for clarity is keeping your personal and business expenses 100% separate. Mixing the two is a common hurdle for 25% of new entrepreneurs, but once you draw that line, your financial picture becomes crystal clear. If you find yourself overwhelmed by these details, reaching out for professional bookkeeping services can turn that stress into a "thank heavens" moment of clarity.

How to Read and Analyze Your P&L for Growth in York and Hanover

Reading your profit and loss statement for small business is about more than checking your bottom line at the end of the month. It's a diagnostic tool that reveals the health of your operations. In South Central Pennsylvania, 74% of service-based businesses experience significant seasonal fluctuations. By comparing your June 2024 data against June 2023, you can determine if a revenue dip is a local market trend or an internal issue. Vertical analysis helps here; it turns every line item into a percentage of your total sales. If your cost of materials was 25% of revenue last year but jumped to 32% this quarter, you've identified a specific area where inflation or waste is eating your profit.

- Trend Tracking: Look at a 12-month rolling view to see if your growth is steady or erratic.

- Money Leaks: Identify recurring subscriptions or vendor fees that have crept up by 5% or 10% without notice.

- Seasonality: Prepare for the typical 30% revenue drop many Hanover retailers face in February by building a cash reserve in October.

Spotting Red Flags in Your Financial Reporting

A major red flag occurs when your expenses grow at 1.5x the rate of your revenue. This imbalance suggests that scaling your business is actually making you less profitable. You should also watch your "miscellaneous" category. If this bucket exceeds 2% of your total spending, your reporting has become "foggy." This lack of detail hides waste and makes it impossible to find tax savings. Inconsistent coding, such as labeling a software fee as "Office Supplies" one month and "Dues" the next, creates a 20% margin of error in your year-end projections. Professional bookkeeping in Hanover, Pennsylvania ensures every penny has a consistent home.

Using Your P&L to Set Realistic Goals

Your profit and loss statement for small business provides the data needed to make brave moves. If you want to hire a new technician at a $50,000 annual salary, your P&L will show if your current net profit margin can absorb that $4,166 monthly cost. Most York County entrepreneurs feel a 40% increase in confidence once they can see their break-even point in black and white. Use your historical data from the last 24 months to build a budget for the next quarter. This clarity transforms your financial stress into a structured plan for expansion.

How to Create a Profit and Loss Statement in 5 Simple Steps

Building a profit and loss statement for small business owners shouldn't feel like a heavy burden. It is a tool designed to give you clarity and freedom. When you understand where your money goes, you regain control over your future. Follow these five steps to transform your raw data into a meaningful financial story.

- Choose your reporting period: Most Hanover business owners find that monthly reports offer the best pulse on their operations. You can also run these quarterly or annually to see long-term trends.

- Gather all sources of income: Collect every invoice, sales receipt, and bank deposit from the last 30 days. This ensures your gross revenue figure is complete.

- Categorize every expense: Group your spending into categories like rent, utilities, and marketing. Using tax-compliant categories now saves you hours of stress during the April tax season.

- Calculate your net income: Subtract your total expenses from your gross profit. This final number tells you exactly what stays in your pocket after the bills are paid.

- Review for accuracy: Look for outliers or missing entries. If the numbers feel confusing, you can always consult a professional to ensure your books are pristine.

Step-by-Step QuickBooks Online Generation

QuickBooks Online makes generating a profit and loss statement for small business growth simple and fast. Start by clicking the "Reports" tab in your left-hand dashboard. Select the "Profit and Loss" standard report from the list. Use the customization tool to set your specific dates, such as the previous month or fiscal year. Finally, choose between Cash and Accrual reporting. Most local service businesses prefer the Cash method because it reflects the actual money currently in their bank account.

The Pitfalls of DIY Manual Entry

Manual spreadsheets often lead to frustration and expensive mistakes. Studies show that 88% of spreadsheets contain significant errors, which can lead to missed tax deductions or incorrect profit reporting. Using QuickBooks allows you to utilize automated bank feeds, which pull your transactions directly into your ledger. This automation prevents the "broken formula" trap that plagues many DIYers. To keep everything perfect, you must prioritize reconciliation. Reconciliation is the essential process of matching your internal records against your bank statements to verify that every single penny is exactly where it should be.

Ready to move from financial chaos to total confidence? Learn how our bookkeeping services provide the relief you deserve.

Achieving Financial Peace with Professional Bookkeeping in Pennsylvania

A clean profit and loss statement for small business owners in Hanover acts as a sanctuary from the noise of daily operations. It transforms rows of confusing numbers into a clear narrative of your success. When those reports are finally accurate and up to date, you'll experience that signature "Thank Heavens" moment. The constant low-level hum of financial anxiety simply disappears. You gain the freedom to lead your team with confidence instead of looking over your shoulder at impending deadlines.

Professional oversight is the most effective shield against the annual tax season panic. Without it, many entrepreneurs spend the first two weeks of April buried in shoe boxes of receipts and unlinked bank transactions. This frantic scramble leads to missed deductions and costly errors. By maintaining an organized back office year-round, you ensure that tax time is just another quiet day on the calendar.

Why a Certified ProAdvisor Makes the Difference

Expert setup is the foundation of every reliable report. Industry data shows that 82% of small businesses fail because of poor cash flow management, often rooted in messy records. A Certified ProAdvisor ensures your accounts are reconciled to the penny from day one. This precision pays for itself; well-maintained books can slash year-end tax preparation fees by $1,500 or more because your CPA won't need to perform a "rescue" cleanup. You can discover our heart for helping local entrepreneurs on the About Thank Heavens Bookkeeping page.

Your Next Steps Toward Financial Freedom

Stop guessing and start knowing. The transition from financial chaos to organized advocate energy happens through a simple, supportive partnership. You don't have to spend 6 hours every weekend trying to categorize transactions in a spreadsheet. By outsourcing these details, you reclaim your time and your peace of mind. Imagine entering the March 15th or April 15th deadlines with every dollar already accounted for and every receipt filed.

We invite you to a free consultation to map out your path to clarity. Let's work together to ensure your profit and loss statement for small business growth reflects the hard work you put in every single day. You deserve a partner who finds joy in the details so you can find joy in your business again.

Take Control of Your Hanover Business Growth Today

Your financial data shouldn't be a source of stress. By mastering the 5 simple steps to create a profit and loss statement for small business, you move from guessing to knowing exactly where your money goes each month. You now understand how to break down revenue and expenses to find hidden growth opportunities right here in York and Hanover. This clarity is the foundation for every confident decision you'll make for your company's future. Having a clear view of your net income allows you to plan for 2024 and beyond with absolute certainty.

You don't have to carry the burden of monthly reconciliations or complex cleanups alone. As a Certified QuickBooks Online ProAdvisor with deep roots in the Hanover, PA community, I specialize in restoring order to messy books and providing the steady support you need. Whether you're catching up on 12 months of record-keeping or need precise monthly reporting, we'll transform your financial chaos into a state of total calm. You deserve to focus on your passion while we handle the meticulous details of your back office with care. Your peace of mind is just one conversation away.

Ready for financial clarity? Schedule your "Thank Heavens" consultation today!

You've worked hard to build your legacy in Pennsylvania, and having a partner who cares about your success makes all the difference. We can't wait to help your business thrive.

Frequently Asked Questions

Is a Profit and Loss statement the same as an Income Statement?

Yes, a P&L statement and an Income Statement are two names for the exact same financial report. Whether you call it a P&L or an Income Statement, this document summarizes your revenue, costs, and expenses over a specific period. It's the primary tool used to measure your 12 month profitability. Most Hanover business owners use these terms interchangeably when discussing their performance with lenders or tax professionals.

How often should a small business in Hanover review its P&L?

You should review your profit and loss statement for small business at least once every 30 days. Monthly reviews allow you to spot 5% fluctuations in spending before they become 50% losses. If you only look at your numbers once a year at tax time, you miss 11 months of opportunities to adjust your strategy. Regular check-ins provide the clarity you need to make confident hiring or purchasing decisions.

Can I create a P&L statement if I haven’t kept good records all year?

Yes, you can reconstruct your financial history even if your records are currently in a shoebox. We start by gathering 12 months of bank statements and credit card history to categorize every transaction. It's a meticulous process, but it turns 365 days of chaos into an organized roadmap. This cleanup usually takes about 15 to 20 hours for a typical service-based business, finally giving you the freedom to move forward.

What is the difference between cash and accrual P&L statements?

The difference lies in when you record your income and expenses. Cash basis records a transaction the moment money enters or leaves your bank account. Accrual basis records it the moment you send an invoice or receive a bill, even if the 100% payment hasn't cleared yet. About 85% of small businesses start with the cash method because it's simpler to track and mirrors your actual bank balance more closely.

Why is my net profit different from the cash in my bank account?

Your net profit rarely matches your bank balance because of non-cash expenses like $2,000 in annual depreciation or principal payments on loans. Your P&L shows your business performance, while your bank account shows your liquidity. If you spent $5,000 on new equipment, that cash is gone, but the full expense doesn't appear on your P&L immediately. This gap is why 3-way reconciliation is vital for your peace of mind.

Does a P&L statement show my business debt or loans?

No, the total amount of your debt or the principal balance of a loan appears on your Balance Sheet, not your P&L. Your profit and loss statement for small business only records the interest portion of your loan payments as an expense. If you pay $1,200 toward a truck loan, only the interest amount reduces your profit. Tracking this correctly ensures your tax obligations are accurate and your financial health is clear.

What are the most common P&L mistakes for new small businesses?

Mixing personal and business expenses is the most frequent error, affecting 60% of new entrepreneurs. Another common mistake is recording a $1,500 equipment purchase as an expense rather than an asset. These errors distort your true profitability and create stress during tax season. Establishing a dedicated business account from day one helps you maintain 100% clean records and provides the sanctuary of organized finances.

How much does it cost to have a professional prepare my monthly P&L?

Professional monthly bookkeeping for a Hanover small business typically ranges from $300 to $800 per month depending on your transaction volume. This investment buys you much more than a report; it buys you 10 hours of your time back and the confidence that your books are perfect. When you outsource this task, you replace financial anxiety with a steady, predictable rhythm of clarity that allows your business to thrive.